Global Video Game Market

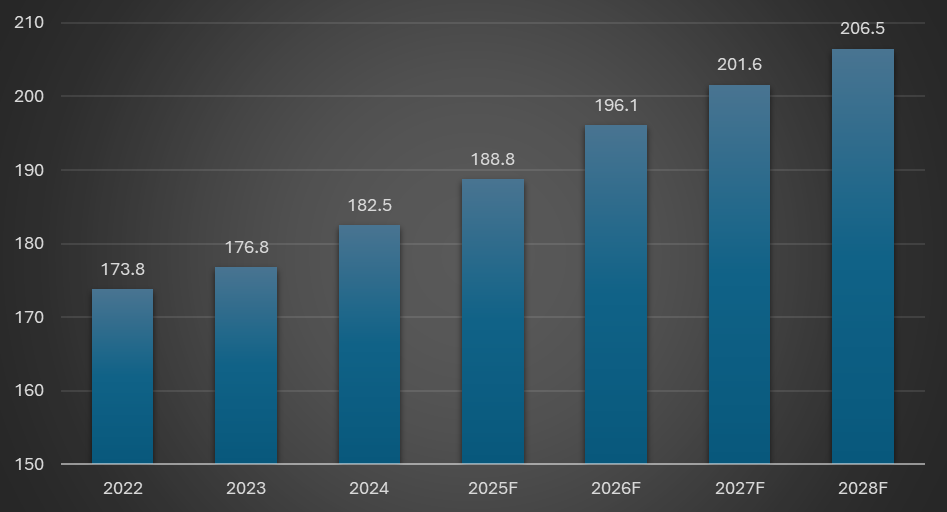

According to analysts from the research company Newzoo, the global games market generated revenues of USD 182.5 billion in 2024, representing sector growth of 3.2% year-on-year.

The main growth drivers were:

- dynamic growth of the mobile segment in regions where handheld devices remain the dominant platform — especially in Latin America, the Middle East and Africa,

- stable sales of games and digital services in North America and Europe,

- new title releases,

- more effective monetization of the existing player base.

According to Newzoo’s forecasts, industry revenues are expected to increase to USD 206.5 billion by 2028, with a compound annual growth rate, CAGR, of approximately 3.1% in 2024–2028.

This means that the games market is expected to grow faster than in 2022–2024, when CAGR amounted to 2.5%. However, analysts emphasize that the global sector is entering a maturity phase, in which player retention and innovative forms of monetization are becoming increasingly important.

Chart 1. Value of the global video game market in 2022–2024 and forecast until 2028

Data in USD billion

Source: Global Games Market Report, Newzoo, 2025.

Mobile Segment

The largest segment of the global games market in terms of revenue in 2024 remained mobile games, including smartphones and tablets.

After a series of declines in previous years, this segment finally recorded a year of growth. According to Newzoo data, its value reached approximately USD 100.4 billion, representing growth of approximately 5% year-on-year.

Mobile games therefore accounted for 55% of global industry revenues.

According to Newzoo specialists, the highest-grossing titles of 2024 are expected to maintain good performance in 2025, although a gradual slowdown will be visible due to the aging of game titles.

One of the key challenges remains the discoverability of new productions. The app and online store market is oversaturated, while content is increasingly fragmented across different platforms. As a result, more selective game catalogues may emerge to make it easier for players to access high-quality titles.

In the coming years, mobile games will remain the dominant segment of the games market, both in terms of consumer spending and total revenue value.

Console Segment

The second-largest segment of the global games market is consoles. According to Newzoo estimates, revenues from this segment amounted to approximately USD 43.8 billion in 2024, representing a decline of approximately 1% year-on-year.

Analysts forecast, however, that the coming years will bring a clear rebound. In 2025, the console market is expected to grow by 5.5% year-on-year, with the highest growth dynamics recorded in the Asia-Pacific region, driven primarily by Japan.

High growth of 5.4% year-on-year is also expected in North America.

Several factors are contributing to the improvement in the segment’s results. One of them is the launch of Nintendo Switch 2 on 5 June 2025, which provides an impulse for revenue growth after a period of slowdown in the late life cycle of the previous console generation.

Rising software prices, which support higher sales value, are also significant. Major game releases planned for 2025 will also support the segment’s performance.

The strongest growth is forecast in regions where Nintendo Switch has been particularly popular, especially in East Asia and France.

According to data as of 11 September 2025, the total cumulative sales of PlayStation 5, Xbox Series S/X, Nintendo Switch and Nintendo Switch 2 consoles amounted to 270.01 million units.

Table 19. Cumulative Number of Console Units Sold

| Console | Console Launch Date | North America | Europe | Japan | Rest of the World | Total |

|---|---|---|---|---|---|---|

| Nintendo Switch | 03.03.2017 | 53.13 | 39.02 | 35.92 | 23.28 | 151.35 |

| PlayStation 4 | 15.11.2013 | 38.12 | 45.86 | 9.68 | 23.53 | 117.20 |

| Xbox One | 22.11.2013 | 32.97 | 14.86 | 0.12 | 10.02 | 57.96 |

| PlayStation 5 | 12.11.2020 | 29.14 | 26.79 | 6.95 | 15.34 | 78.22 |

| Xbox Series X/S | 11.10.2020 | 18.68 | 8.54 | 0.68 | 5.50 | 33.40 |

| Nintendo Switch 2 | 05.06.2025 | 2.29 | 1.53 | 1.70 | 1.52 | 7.04 |

Source: Issuer’s own compilation based on VGChartz, as of 11 September 2025.

PC Games Segment

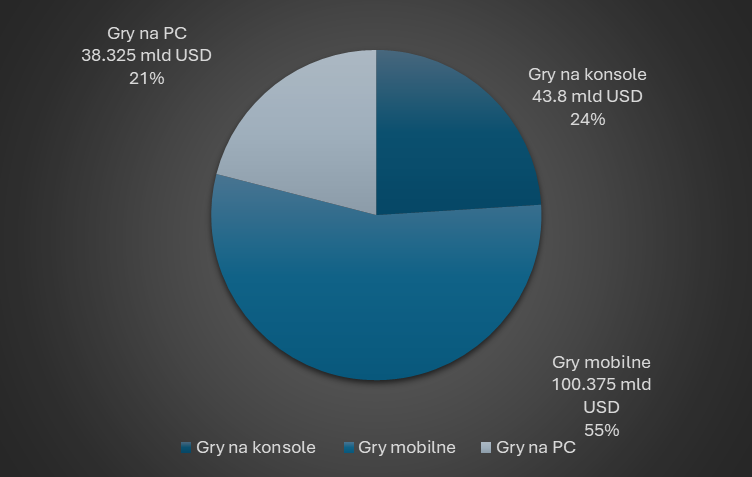

The next segment of the games market in terms of revenue is PC games, which accounted for approximately 21% of the global market in 2024.

Experts from Newzoo estimate that revenues in this segment amounted to approximately USD 38.3 billion, representing growth of approximately 3% compared with the previous year.

The result was mainly influenced by releases of popular titles such as Palworld and Helldivers 2, which achieved very strong sales results.

Forecasts for 2025 anticipate global PC market growth of 2.5% year-on-year. The fastest growth is expected in smaller markets in the Middle East and Africa, while the Asia-Pacific region is expected to achieve growth of 3.1%.

Similar growth is forecast in China, driven by the growing popularity of Steam, revenues from 2024 releases, returning Activision Blizzard titles, and activity in esports.

Growth in the segment in 2025 will be supported by a stronger release calendar in the first half of the year, including long-awaited and highly rated productions such as Monster Hunter Wilds, Kingdom Come: Deliverance II and Assassin’s Creed Shadows, as well as numerous smaller titles.

Despite strong releases at the beginning of 2025, the pace of revenue growth in the PC segment is expected to slow slightly, as a significant portion of 2025 revenues will come from games that already achieved success in 2024, as well as due to declining sales of established titles such as League of Legends, Rainbow Six: Siege and Apex Legends.

Chart 2. Global Games Market Revenue in 2024 by Platform

Data in USD billion and %

Source: Global Games Market Report, Newzoo, 2025.

Geographic Structure of the Global Games Market

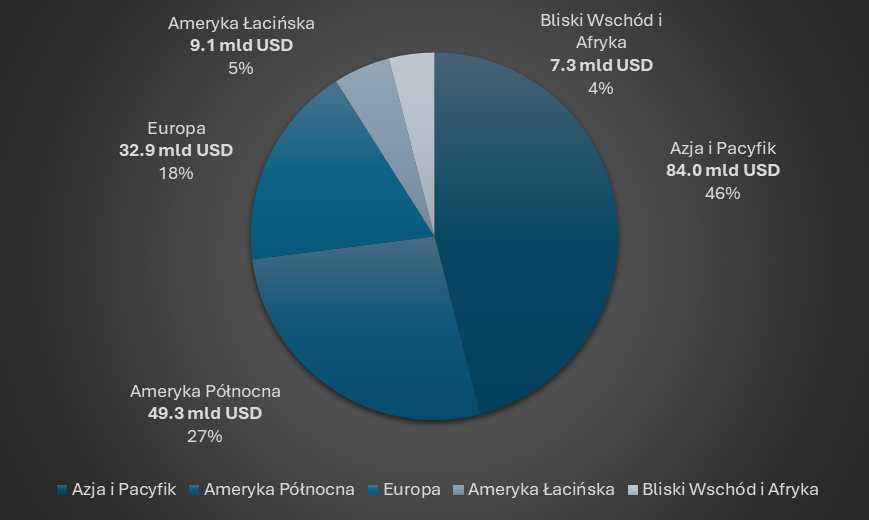

In geographic terms, the most profitable region for the video game industry in 2024 remained Asia-Pacific, which generated USD 84 billion, or approximately 46% of total global games revenue.

The following regions ranked next:

- North America — approximately 27%,

- Europe — approximately 18%,

- Latin America — approximately 5%,

- Middle East and Africa — approximately 4%.

In the coming years, the fastest-growing regions in the world in terms of games revenue are expected to be the Middle East and Africa, Latin America, and North America.

Chart 3. Share of Individual World Regions in the Video Game Market Structure in 2024

Source: Global Games Market Report, Newzoo, 2024, 2025.

According to Newzoo analysts, in 2025 the global games market is expected to grow at different rates across regions.

In the Asia-Pacific region, revenues are expected to increase by approximately 2.3% year-on-year, although local nuances mean that growth dynamics will be uneven.

In North America, the market is expected to grow by approximately 4.2% year-on-year, supported, among other things, by the stable console segment.

In Europe, the growth rate is expected to reach approximately 3.6% year-on-year; however, demographic constraints, such as population aging and lower population growth, will limit further development.

Younger markets are expected to develop the most dynamically. Latin America is forecast to record growth of approximately 6.4% year-on-year, supported by a rapid increase in the number of players across all platforms, although consoles will remain behind.

Even higher growth, at approximately 7.5% year-on-year, is expected in the Middle East and Africa, where the mobile segment in particular will become the main growth driver. This is due to the dynamic development of Chinese OEMs, or Original Equipment Manufacturers, such as Xiaomi and Realme, which leverage affordability, local production and saturation of the retail market.

Number of Active Players Worldwide

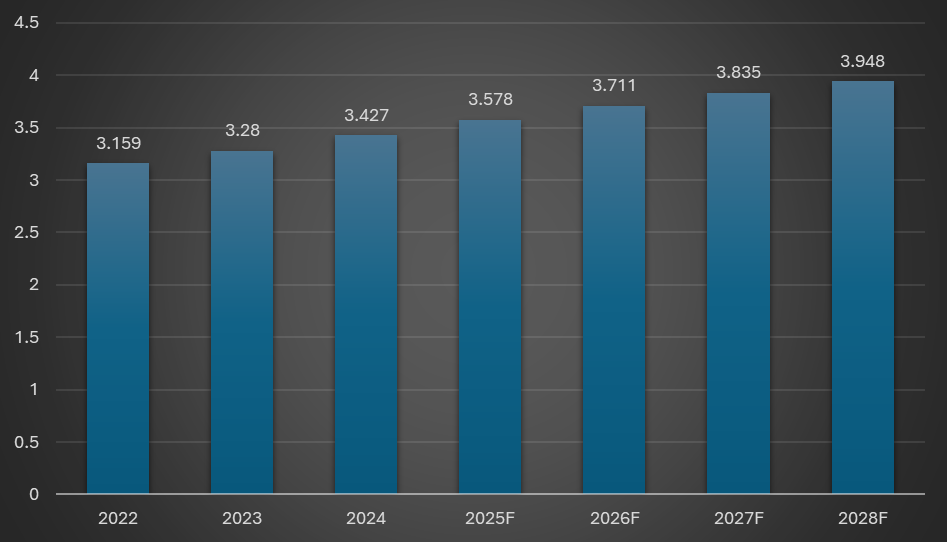

According to Newzoo, at the end of 2024 there were approximately 3.427 billion active players worldwide, with mobile players consistently representing the largest group.

According to analysts’ forecasts, in 2025 this number is expected to grow by approximately 4.4% to 3.578 billion players, of which mobile players will account for approximately 83%, or 2.985 billion.

The PC games segment will rank second, with 0.936 billion players, or 26%, while the number of active console players in 2025 is expected to amount to approximately 0.645 billion.

According to Newzoo specialists’ forecasts, by the end of 2028 the number of players is expected to increase to 3.948 billion, which represents growth of approximately 25% compared with 2022.

The compound annual growth rate, CAGR, in 2024–2028 is expected to amount to approximately 3.60%.

According to Newzoo, the largest number of players at the end of 2025 will come from Asia — approximately 53%. The following regions will rank next:

- Middle East and Africa — approximately 16%,

- Europe — approximately 13%,

- Latin America — approximately 11%,

- North America — approximately 7%.

The total number of players in 2025 is expected to represent 61.5% of the online population, which is forecast to grow by 3.8% year-on-year to 5.8 billion.

This means that the majority of the world’s population with Internet access will play games on at least one platform, with most of them playing on mobile devices.

Forecasts indicate that the share of players in relation to the online population will remain stable in 2025–2028, confirming the maturity of the games market and the need to monetize the existing audience base.

Chart 4. Number of Active Video Game Players Worldwide in 2022–2024 and Forecast for 2025–2028

Data in billions

Source: Global Games Market Report, Newzoo, 2025.

Polish Video Game Market

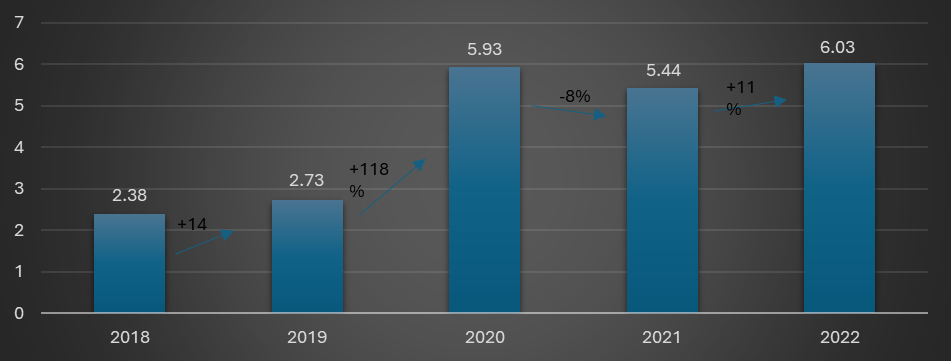

According to data included in The Game Industry of Poland report, revenues of the games sector in Poland reached a record EUR 1.29 billion in 2022.

This means that after a decline of 8% year-on-year in 2021, growth of 11% year-on-year was recorded in 2022.

Taking into account the high sector revenues in 2020 related to the release of Cyberpunk 2077 by CD Projekt S.A., as well as the fact that the global games market recorded a year-on-year decline in 2022, analysts consider this result satisfactory.

The value of the Polish consumer market increased by 15% year-on-year in 2022 and amounted to USD 1.23 billion, placing it 19th globally.

This also means that Poland is one of the fastest-growing countries in this respect. It is estimated that by 2026 the value of the Polish consumer market will reach USD 1.6 billion.

Chart 5. Revenue Value of Polish Entities from the Games Sector

Data in PLN billion

F — forecast.

Source: The Game Industry of Poland report, 2023.

Poland as a Producer of PC Games

Poland is one of the global leaders in the production of PC games, most of which are distributed through the Steam platform.

On Steam’s Top 200 wishlist, i.e. the ranking of the most anticipated titles, Poland ranked first in the world in January 2021 with 47 games.

As at the date of preparation of the report, approximately 30 Polish games were included on the above-mentioned list.

In total, the industry releases more than 530 new game editions each year across more than a dozen platforms.

In 2022, most games from Polish studios were released for personal computers. During that period, 162 titles debuted, accounting for nearly one-third of all releases.

Nintendo Switch ranked second in terms of the number of releases, with 92 new titles, representing approximately 17% share.

A slightly smaller number of games was released for mobile devices — 90 releases.

The following platforms ranked next:

- Xbox One — 52 releases,

- PlayStation 4 — 42 releases,

- PlayStation 5 — 28 releases,

- VR — 25 releases.

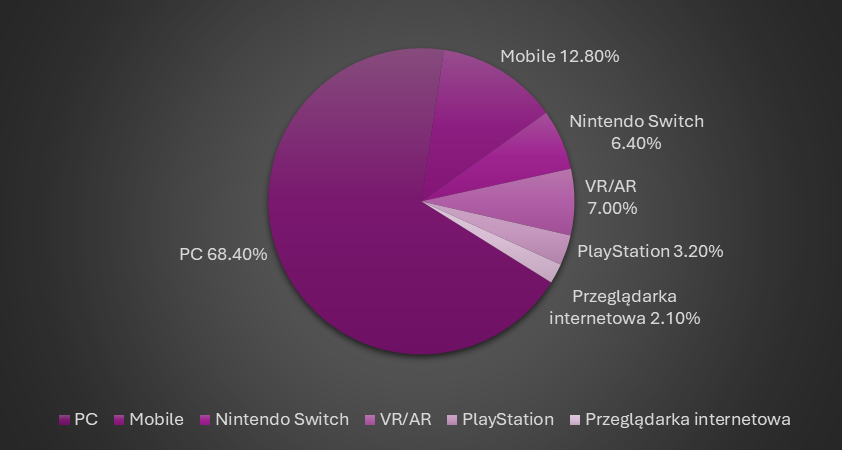

The above data results from the fact that 68.4% of Polish video game producers indicated PC as the main platform for which they create games.

Mobile devices were indicated by 12.8% of Polish studios. VR ranked next with a 7% share, followed by Nintendo Switch with a 6.4% share.

Chart 6. Main Platforms Declared by Polish Development Studios

Source: The Game Industry of Poland report, 2023.

Number of Studios and Employment in the Polish Games Industry

In May 2023, there were approximately 494 game producers and publishers operating in Poland.

The number of studios has practically stopped growing after doubling over the past ten years. It is not yet clear whether this number has reached a stabilization point from which it will begin to grow again after certain criteria are met, or whether a decline in the number of studios should be expected.

Nevertheless, rotation is still visible. New companies are established every year, with stronger foundations than in the past, but generally they replace businesses that are being liquidated. As a result, this no longer contributes to the overall increase in the number of companies in the industry to the same extent as before.

The report also indicates growth in the number of employees in the Polish games industry, which since 2017 had remained at 23–27% year-on-year.

Currently, the growth rate is 16%, which remains an impressive result and one of the best outcomes among games industries of comparable size.

Employment in the games sector in Poland exceeds 15,000 people, which means that Poland significantly exceeds the German sector in this respect.

A high share of women in the industry was also recorded, making Polish gamedev an attractive place for talent from all over the world.

Key Sales Markets for Polish Games

The most important regions for the sale of Polish games are:

- North America,

- Europe,

- Asia.

Each of these continents accounts for 20% to 40% of total sales, depending on the popularity of a given title.

In general, the continents of the Northern Hemisphere account for 75–90% of total sales of games from Poland.

The largest markets for Polish games are the USA and China. In the case of Polish games, one of these countries usually dominates, generating 20% to 40% of total sales revenue.

The entire European Union may have a comparable share in sales. However, the countries that most often appear in top rankings of markets for Polish games are three European countries:

- the United Kingdom,

- Germany,

- France.

Players in Poland and Spending Structure

The number of players in Poland is estimated at 17 to 20 million.

Players in Poland range from the most dedicated users to those who play only occasionally or for social interaction.

It should be noted that the Polish games market is dominated by PC games, whose share continues to grow. Poland is the second-strongest market in terms of the number of PC players per capita, just behind Canada.

The number of active Polish players on Steam is estimated at 3 to 4 million.

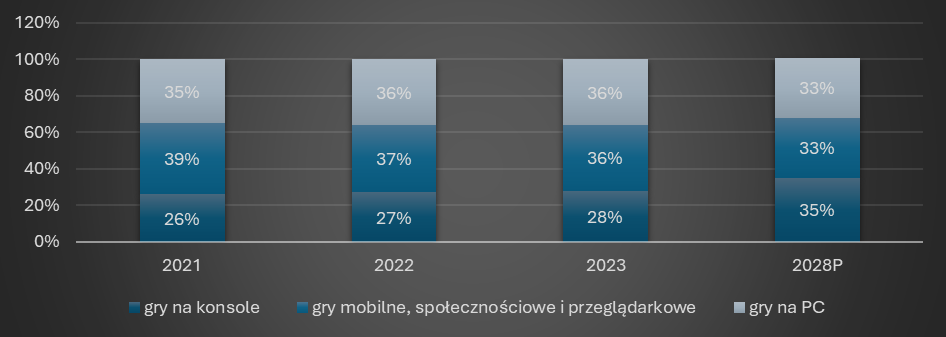

According to the PMR report, however, significant changes in the market structure are expected in the coming years. Consumer spending on console titles is expected to grow the fastest. Their share is expected to reach 35% by 2028, compared with 27% in 2022.

Chart 7. Structure of Spending on Video Games in Poland

Data in %

Source: PMR, 2023.

Purchasing Platforms in Poland

The most popular purchasing platform among PC players in 2020 remained Steam, with a 38% share.

Its popularity is influenced by its long presence on the Polish market and numerous promotions, which Polish players readily use.

Origin ranked second, with 13% of respondent indications.

Auction services such as Allegro, eBay and OLX were only slightly less popular, receiving 12% of indications.

Microsoft Store and Epic Games Store each received 6% of respondent indications.

Domestic platforms for trading electronic versions of games, such as G2A, Uplay and Kinguin, were much less popular.

Research also indicates that 57% of respondents download free games from the Internet.

Moreover, traditional game distribution still had more supporters — 46%, while digital distribution accounted for 40%.